Market update – resilience amid uncertainty

Markets continued to recover over the month, with stronger returns across the Dynamic Planner benchmarks, reflecting improving investor sentiment and a renewed willingness to engage with risk assets. While geopolitical and macroeconomic uncertainty remained firmly in the background, markets increasingly appeared willing to look through near-term disruptions and refocus on underlying economic and corporate fundamentals. The recovery was not uniform, however, with performance concentrated across selected regions and asset classes.

Risk appetite returns, led by equities

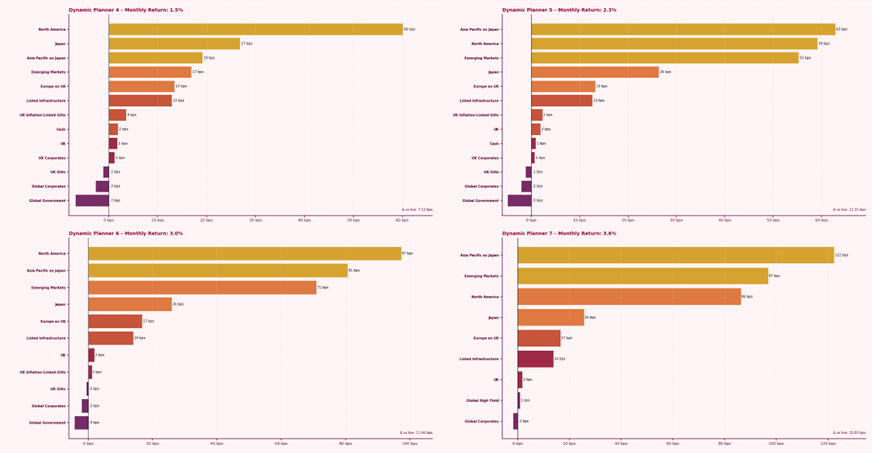

Higher-risk Dynamic Planner benchmarks generally experienced stronger returns during the month, reflecting their greater exposure to global equity markets and growth-oriented assets. North America remained an important contributor across the range, supported by continued strength in US equities. Asia Pacific ex Japan and Emerging Markets also provided meaningful positive contributions, particularly within higher-risk portfolios, suggesting that improving sentiment broadened beyond the US and into other regions. Japan contributed positively, while Europe ex UK remained more subdued.

The clearest illustration of improving sentiment was the resilience shown in US equities, with the S&P 500 reaching fresh record highs despite the unsettled backdrop. Rather than signalling the disappearance of risk, this suggested investors increasingly looked through near-term shocks and refocused on earnings expectations and longer-term growth themes.

Figure 1: Dynamic Planner benchmark attribution highlights regional equity leadership, particularly across North America, Asia Pacific ex Japan and Emerging Markets.

Fixed income offers limited protection

While equities recovered, fixed income provided more limited support. UK bonds, gilts and inflation-linked gilts detracted across much of the benchmark range, reflecting the continued influence of higher yields and evolving policy expectations. Alongside geopolitical developments, investors also remained focused on fiscal pressures and the implications of elevated government borrowing, which continued to weigh on bond markets.

Unlike more conventional risk-off periods, government bonds did not provide broad defensive support, reinforcing the theme that diversification behaved differently during this period. This meant that while diversified portfolios remained more resilient than concentrated exposures, the traditional negative relationship between equities and bonds proved less dependable than investors might typically expect.

Markets absorb the shock

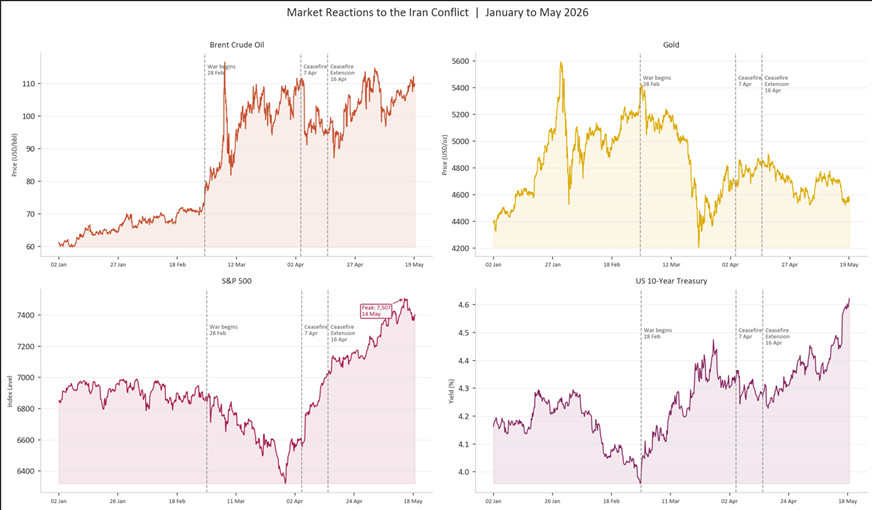

Recent market behaviour also highlighted the continued influence of exogenous shocks — events that sit largely outside the scope of standard economic modelling and forecasting frameworks. Geopolitical developments remained an important backdrop throughout the period, with markets reacting sharply to developments surrounding the Iran conflict and subsequent ceasefire discussions. Oil prices reflected supply concerns and geopolitical risk premia, while gold initially benefited from safe-haven demand before sentiment began to stabilise.

At the same time, equity markets demonstrated notable resilience. Initial risk-off reactions gradually faded as fears of sustained escalation eased and diplomatic efforts emerged, highlighting how quickly markets can reassess geopolitical risk when expectations begin to shift. Cross-asset reactions remained uneven throughout, with safe-haven flows rotating between gold and bonds rather than settling into a single defensive trade.

Figure 2: Market reactions to the Iran conflict illustrate how geopolitical developments influenced oil, gold, equities and bond markets.

Looking ahead

While market conditions have stabilised compared with earlier periods of volatility, conviction remains measured. Improving sentiment has supported higher-risk assets, yet markets continue to balance this optimism against an environment still shaped by geopolitical uncertainty, evolving central bank expectations and elevated bond yields. Whether recent gains develop into a broader and more durable recovery may depend on how these competing forces evolve in the months ahead.