Sunil Krishnan from Aviva Investors highlights the key themes for multi-asset investors to monitor in 2024.

Read this blog to understand:

- The potential impact of elections on global markets

- Why the odds of a soft landing for major economies have improved

- How artificial intelligence could improve corporate productivity

- The prospects for stronger growth in China

The decade so far has been a turbulent period for the global economy. The pandemic roiled markets and interrupted the smooth working of supply chains. In February 2022, just as economies started reopening after COVID-19 lockdowns, Russia’s invasion of Ukraine added significant inflationary pressures. Central banks launched an aggressive monetary tightening cycle to tackle rising prices, which radically altered the market landscape. The economic effects are still playing out.

We see scope for further disruption in 2024. Billed as the biggest election year in history, 2024 will bring a sequence of major elections across the world, with the outcome in many cases too close to call. Central banks must decide if and when to cut rates, now that inflation has started to fall in many economies.

The hype surrounding generative artificial intelligence (AI) technology is set to continue, affecting equity markets. And questions remain over China’s economic policies and growth trajectory. So how will these four themes affect investors with a multi-asset focus?

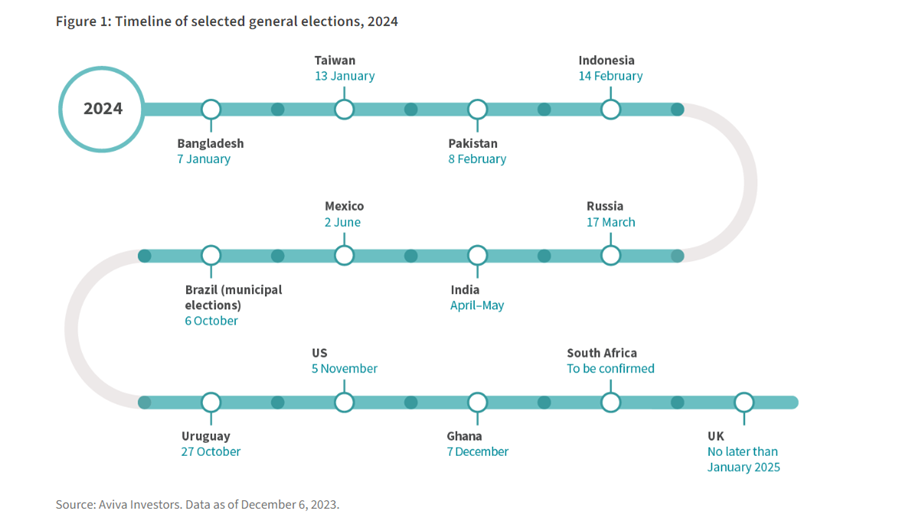

1. Politics will be a dominant theme in 2024, as four billion people – 41 per cent of the world’s population – go to the polls. The US and Taiwanese elections might have the biggest effect on markets

The US, UK, India, Indonesia, Russia, Taiwan: some of the world’s most populous and economically important countries are set for general elections in 2024 – although not all of these votes will be deemed free and fair.

The UK general election is expected towards the end of the year (it could happen as late as January 2025). Our view is that in the possible event of a change in government, this might result in longer-term policy changes – for example on fiscal spending and tax policy – but UK politics will likely not have a big impact on global markets in the near term. The US presidential and Taiwanese elections are potentially more consequential.

In the US, the candidate most likely to disrupt existing economic arrangements is former president Donald Trump, who is running for the Republican nomination and enjoys a strong lead in early polling ahead of the vote in November 2024. This is something investors need to take seriously. Keen to avoid the disorganisation seen in his first term, Team Trump has been busy recruiting aides who can take hold of the agenda from the start. The focus is on areas where the White House has a freer hand to enact change, such as trade policy and regulation.

A key domain where Trump could have a “day-one” effect is climate. He has previously pledged to repeat the first-term US withdrawal from the Paris Agreement and signalled he would unwind the Biden administration’s Inflation Reduction Act (IRA), a significant decade-long programme of spending to support the green transition.

There is also a geopolitical angle. Trump-era foreign policy was erratic and transactional but benefited from a broadly peaceful and stable backdrop. Since then, the world has become more volatile due to the wars in Ukraine and Gaza, alongside China’s more assertive stance in East Asia.

To that end, Beijing is taking a strong interest in the outcome of Taiwan’s presidential election in January, as the ruling party candidate Lai Ching-te faces opponents more open to rebuilding relations with China.

If Lai were to win on a strong anti-China platform, that might motivate Beijing to act. Although it is unclear what such action would entail, it would no doubt be a source of uncertainty and potentially involve other major powers, notably the US. The US has given security guarantees to Taiwan; it would be alarming if those guarantees were to be tested.

Political risk is an ever present for global investors, but the range of possible outcomes appears wider next year. We are likely to see more volatility in popular safe havens, such as gold and the US dollar, around the time of key events.

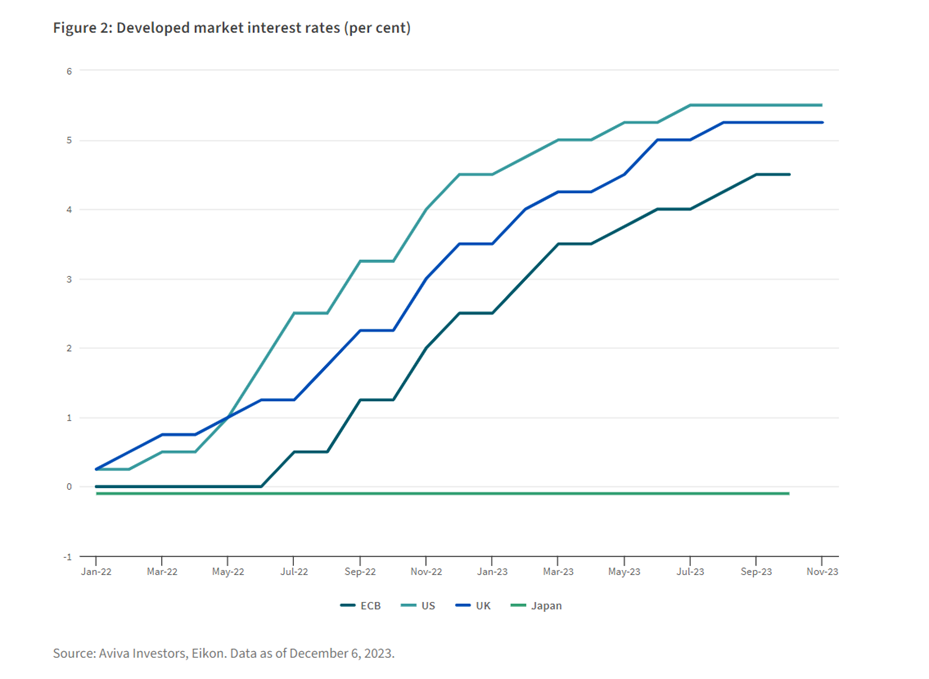

2. The market expectation is for interest-rate cuts across major economies next year. The odds of a “soft landing” are much higher than they were six months ago and 2024 is likely to be a better year for bond returns

Market expectations are for five interest rate cuts in the US and euro zone in 2024, and three in the UK.

These expectations are based on two factors. Firstly, the consensus is that inflation in most regions will still be ahead of central bank targets, but much closer to those targets than today. Secondly, because interest rates have been rising for a while, this may have a braking effect on economic activity and central banks may need to cut rates to support growth.

It is reasonable to think we are at the peak for interest rates, but it is still sensible to be cautious about how quickly they might fall. Even forecasts that have inflation coming down still anticipate core inflation will be above headline inflation. If we get any shocks or volatility in commodity prices, key drivers of headline inflation, allied to above-target core inflation, we could potentially end up with positive inflation surprises. This is not our central case but in such a scenario, expected cuts in rates may not materialise. The risk may be underappreciated by markets.

Nevertheless, the slowing of inflation has increased the odds of a soft landing, which are now much higher than six months ago. The economic data varies between countries, however. Earlier this year, the US saw a slowdown in its housing market and is now seeing a moderation in the jobs market. Wages have slowed but are still strong relative to history. Overall, while tighter monetary policy is having an effect, the signs for growth are not alarming. The base case is that the rise in the unemployment rate will be less than one per cent (although it should be noted that it is difficult, when an economy starts to slow, to keep unemployment under control).

In the euro zone, slowing growth has been more evident in the industrial manufacturing sectors, perhaps connected to reduced demand from a sputtering Chinese economy and challenges in the construction and real estate sectors.

The outlook for inflation and interest rates should allow for a better period for government bonds in 2024

All things considered, the outlook for inflation and interest rates should allow for a better period for government bonds in 2024. The last three years have seen cumulative negative returns for bond markets, which has led investors to question their role in a diversified portfolio.

However, two important things have happened. Firstly, yields on bonds have risen, particularly on longer-dated bonds. Secondly, now that we are approaching the end of the tightening cycle, cash may not offer the high returns it does currently for much longer.

The ideal time for bonds is when there is a sharp drop-off in growth and challenges for risk assets. The combination of peaking interest rates and the extra yield on offer in bonds may attract investors looking to lock-in higher yields for a longer period, rather than be faced with reinvestment risk from holding cash.

3. AI could allow a broader range of companies to significantly improve productivity, supporting global equity markets

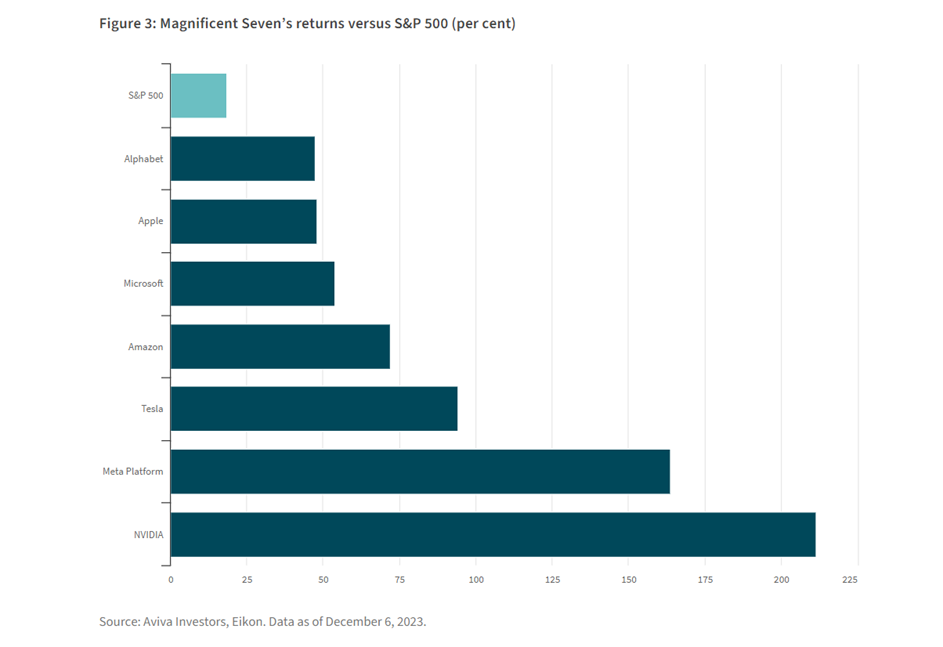

Revenues were a key concern for equity investors in 2023. The big unknown was the extent to which central bank tightening would affect people’s willingness to spend on companies’ goods and services.

The reality is that it was a decent year for global equities, underpinned by continued strength in corporate revenues. There were also concerns about costs, bearing in mind the strong rise in commodity and labour prices, but profit margins held up reasonably well. In the second half of the year, large companies even managed to expand those margins. However, the contribution to overall market returns from the biggest tech companies – whose revenues stand to benefit from the advent of generative AI – has been significant.

Looking ahead to next year, a soft landing, particularly when accompanied by lower borrowing costs, would be a favourable outcome for many companies. But AI is likely to remain a significant factor in market performance. This technology is not going away; the question is whether the gains will be spread beyond a clutch of leaders in Silicon Valley. If AI leads to better productivity among a wider range of companies, that could help profitability and boost equity markets across the board.

One trend across the world since the Global Financial Crisis has been a steady decline in productivity – which creates challenges for companies in terms of how they maintain profits.

In the medium-term, the rollout of AI, along with other major technological advances in areas like healthcare, could reinvigorate productivity and open up the potential for continued profit growth among companies, without necessarily being accompanied by a significant reacceleration of inflation. While this is likely to be a medium-term story, we may start seeing signs of these trends shaping the fortunes of individual stocks in 2024.

4. China’s growth might accelerate next year, but concerns around property and demographics remain

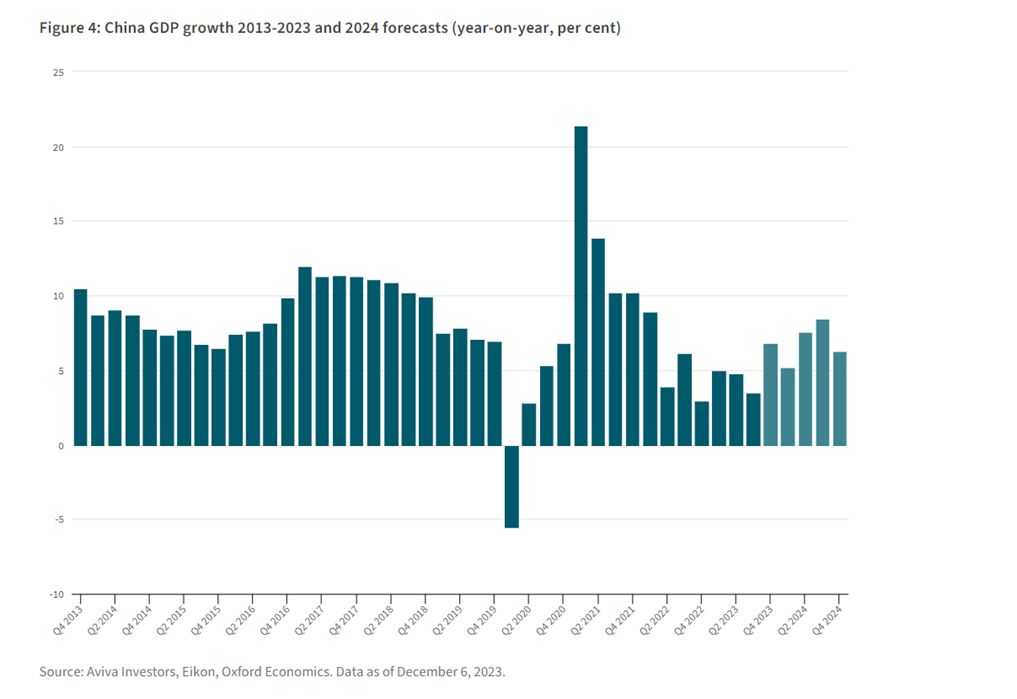

The failure of China to show a meaningful recovery in economic growth was one of the biggest surprises of 2023. In late 2022, there was a strong consensus among investors that China would see a significant resurgence in activity with its post-COVID reopening, after the government imposed stringent lockdowns throughout the pandemic. But the reality has been disappointing. Despite the People’s Bank of China stressing in November the country was still on course to hit its full-year GDP growth target of five per cent, many in the market had hoped for more.1

There are two main reasons for this. Firstly, state intervention in the corporate sector has led to big challenges in terms of foreign direct investment into China. The number of international companies looking to make physical investments into China has dropped quite steeply.

Secondly, China is struggling with ongoing problems in the heavily indebted property sector. We have not seen a meaningful recovery in sales activity and prices since the pandemic. This has financial implications for property developers, which rely heavily on forward sales of houses for liquidity, and local governments, which depend on land sales to boost revenues.

Beijing has introduced many small measures to support the property market, but they have not been effective. This has raised the question of whether China has now essentially put economic growth and prosperity onto the backburner in favour of other priorities, like national security and reducing financial leverage.

While we shouldn’t forget the lasting impact of China’s focus on non-economic objectives, we are probably approaching a stage where the pace of economic stimulus is likely to increase rather than decrease into the new year. We expect the authorities will put more capital to work to support growth and perhaps ease off on some of their concerns about financial leverage and speculation.

More stimulus and faster Chinese growth would support global demand in the short-to-medium term, particularly among emerging markets. However, longer-term challenges around the property sector and rapidly ageing demographics are not going away. We would expect to see them re-emerge as dominant themes after any early sugar-rush from stimulus measures.

Reference

Important information

THIS IS A MARKETING COMMUNICATION

Except where stated as otherwise, the source of all information is Aviva Investors Global Services Limited (AIGSL). Unless stated otherwise any views and opinions are those of Aviva Investors. They should not be viewed as indicating any guarantee of return from an investment managed by Aviva Investors nor as advice of any nature. Information contained herein has been obtained from sources believed to be reliable, but has not been independently verified by Aviva Investors and is not guaranteed to be accurate. Past performance is not a guide to the future. The value of an investment and any income from it may go down as well as up and the investor may not get back the original amount invested. Nothing in this material, including any references to specific securities, assets classes and financial markets is intended to or should be construed as advice or recommendations of any nature. Some data shown are hypothetical or projected and may not come to pass as stated due to changes in market conditions and are not guarantees of future outcomes. This material is not a recommendation to sell or purchase any investment.

The information contained herein is for general guidance only. It is the responsibility of any person or persons in possession of this information to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. The information contained herein does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorised or to any person to whom it would be unlawful to make such offer or solicitation.

In the UK, this document is issued by Aviva Investors Global Services Limited. Registered in England No. 1151805. Registered Office: St Helens, 1 Undershaft, London EC3P 3DQ. Authorised and regulated by the Financial Conduct Authority. Firm Reference No. 119178. 522850 – 31/12/2025