Recent geopolitical tensions and oil price shocks have triggered significant market volatility, impacting both equities and bonds. Market movements remain highly sensitive to political developments, with uncertainty driving intraday swings and risk sentiment.

March delivered one of the sharper geopolitically driven drawdowns this year, with broad-based declines across the Dynamic Planner Benchmarks. Losses scaled with risk: DP4 fell -4.1% over the month while DP7 declined -6.5% [see chart 1], as weakness in global equities combined with an unusual absence of support from fixed income.

Emerging Markets and Asia Pacific ex Japan were the largest detractors, reflecting sensitivity to energy prices and global risk sentiment [see chart 1]. Developed markets also declined, indicating a broad-based risk-off move, while defensive assets offered relative resilience but did not offset wider losses.

Geopolitics drives markets

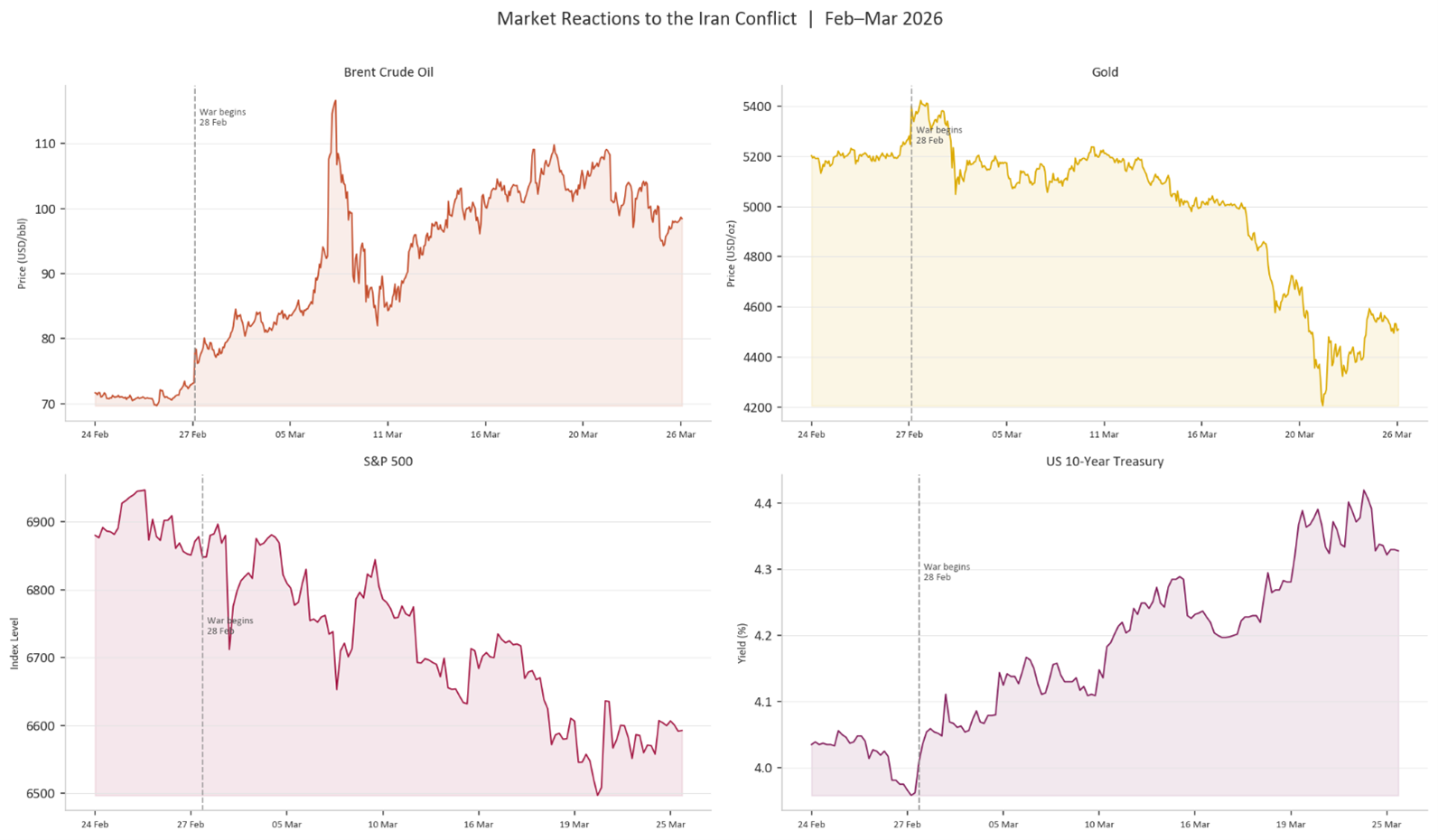

The escalation of tensions at the end of February marked a clear inflection point, triggering an immediate repricing across asset classes [see chart 2]. Rather than the “conventional” risk-off pattern in which bonds rally as equities fall, both declined simultaneously. US 10-year Treasury yields rose by 38bps over the month, even as equities fell by 6%, reflecting inflation pressures rather than the usual flight-to-safety dynamic.

Oil acted as a conduit, linking geopolitical developments to inflation expectations and broader market moves. Brent crude rose sharply from pre-conflict levels, peaking in early March before partially retracing, but remaining elevated overall [see chart 2]. This fed directly into inflation expectations and prompted a repricing of the interest rate outlook, despite no change in central bank policy.

Gold price behaviour reinforced this. Unlike its safe-haven credentials established over the past few quarters, it failed to provide consistent protection, declining after an initial spike. Rising real yields, driven by elevated inflation expectations, reduced the appeal of a non-yielding asset and disrupted relationships investors typically rely on.

The current episode is best understood as a compound shock, part 1970s oil crisis, part post-COVID supply disruption, playing out through a modern lens of fragmented geopolitical signalling. In the 1970s, energy supply disruptions fed directly into inflation and weaker growth, forcing central banks into a painful choice between defending purchasing power and supporting the economy. The post-COVID period offered a more recent demonstration of the same mechanism: supply constraints, initially dismissed as transitory, proved far stickier than expected and kept inflation elevated well after demand had normalised. Today’s environment carries structural echoes of both episodes. What distinguishes it is the additional complexity introduced by political actors sending contradictory signals, alternating between escalatory rhetoric and diplomatic overtures, in a media environment that amplifies each turn in real time. Markets are not simply responding to an oil shock; they are attempting to price a sequence of contingent political outcomes, none of which has yet resolved. That uncertainty premium is itself a source of volatility, independent of the underlying energy fundamentals.

Intraday volatility and market behaviour

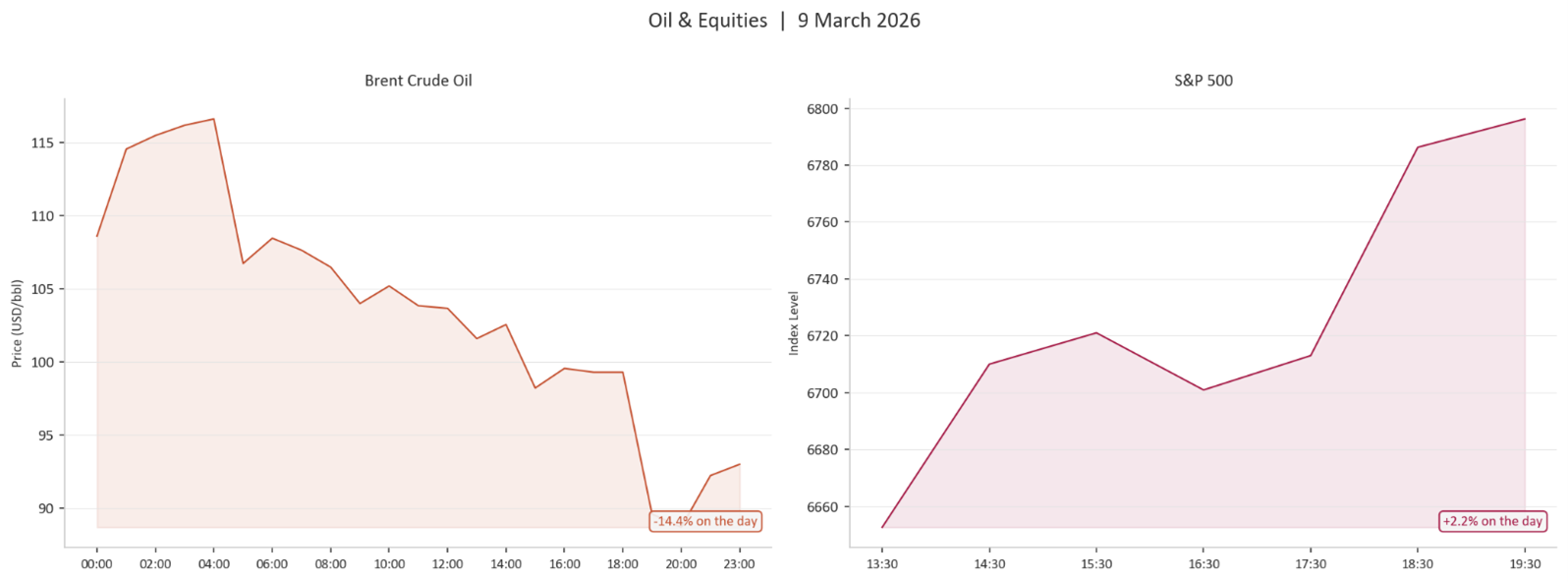

The oil–equity relationship was particularly clear at an intraday level. On 9 March, a sharp decline in oil coincided with a rally in the S&P 500, highlighting how directly energy prices were driving risk sentiment [see chart 3]. As oil retreated on signs of de-escalation, inflation concerns eased and rate cut expectations improved, triggering an immediate equity response. Markets were effectively pricing headlines, with moves driven more by geopolitical news flow than underlying economic fundamentals. This pattern, intraday swings that can appear to contradict the broader trend, is a feature, not a malfunction, of markets navigating genuine uncertainty. When political signals are mixed and sequential — a diplomatic statement in the morning, an escalatory development by afternoon — prices will respond to each in turn, producing intraday moves that can seem inconsistent with the week’s or month’s direction. Short-term price action in this environment should not be read as a reliable signal about market fundamentals; it reflects the market’s real-time attempt to assign probabilities to a rapidly shifting political landscape.

Outlook

The near-term outlook remains tied to oil, and the geopolitics thereof. If prices stabilise, inflation pressures may ease and markets could refocus on growth and monetary policy, with the second-half recovery in March suggesting this may already be underway [see chart 2].

However, renewed escalation would reinforce inflation concerns, constrain the scope for rate cuts and prolong the environment in which both equities and bonds decline together. March highlights how an energy-driven shock can pressure risky assets while weakening the fixed income buffer, leaving limited diversification within a conventional multi-asset portfolio.

Periods of geopolitical disruption feel more disorienting than ordinary market drawdowns precisely because the source of uncertainty lies outside the economic system, beyond the reach of central banks, earnings forecasts, or valuation models. That disorientation is rational; the appropriate response to it is not. History is instructive here. The oil shocks of the 1970s, the Gulf War, the post-COVID supply crisis – each produced sharp drawdowns and considerable anxiety in the moment, yet diversified investors who maintained their allocations through the volatility recovered and ultimately benefited from the subsequent stabilisation. The mechanism that made portfolios resilient then is the same one at work now: diversification across asset classes, geographies, and risk factors does not eliminate short-term drawdowns, but it does prevent any single shock from being permanently destructive. We remain focused on that structural resilience. The current environment does not alter our assessment of the medium-term investment case for well-diversified multi-asset portfolios. Intraday noise is not a reason to act. Staying invested, maintaining discipline, and avoiding reactive positioning decisions remains, as it always has been, the most reliable path through periods like this.