Chart 1

April saw a clear recovery across the Dynamic Planner Benchmarks, with returns increasing alongside risk profiles. DP4 returned 2% over the month, while DP7 rose 5.3% [see chart 1], reflecting a strong equity-led environment in which higher-risk portfolios outperformed.

North America remained the largest contributor across most portfolios, supported by continued strength in US equities. However, the most notable development was the increasing contribution from Emerging Markets and Asia Pacific ex Japan at higher risk levels. In DP6 and DP7, these regions became dominant drivers of performance, highlighting a meaningful broadening in market leadership.

Despite the challenging backdrop, the behaviour of the Dynamic Planner Benchmarks remained consistent with expectations. Performance through both the period of escalation and the subsequent recovery scaled with risk, highlighting the role of diversification across asset classes and regions.

From escalation to stabilisation

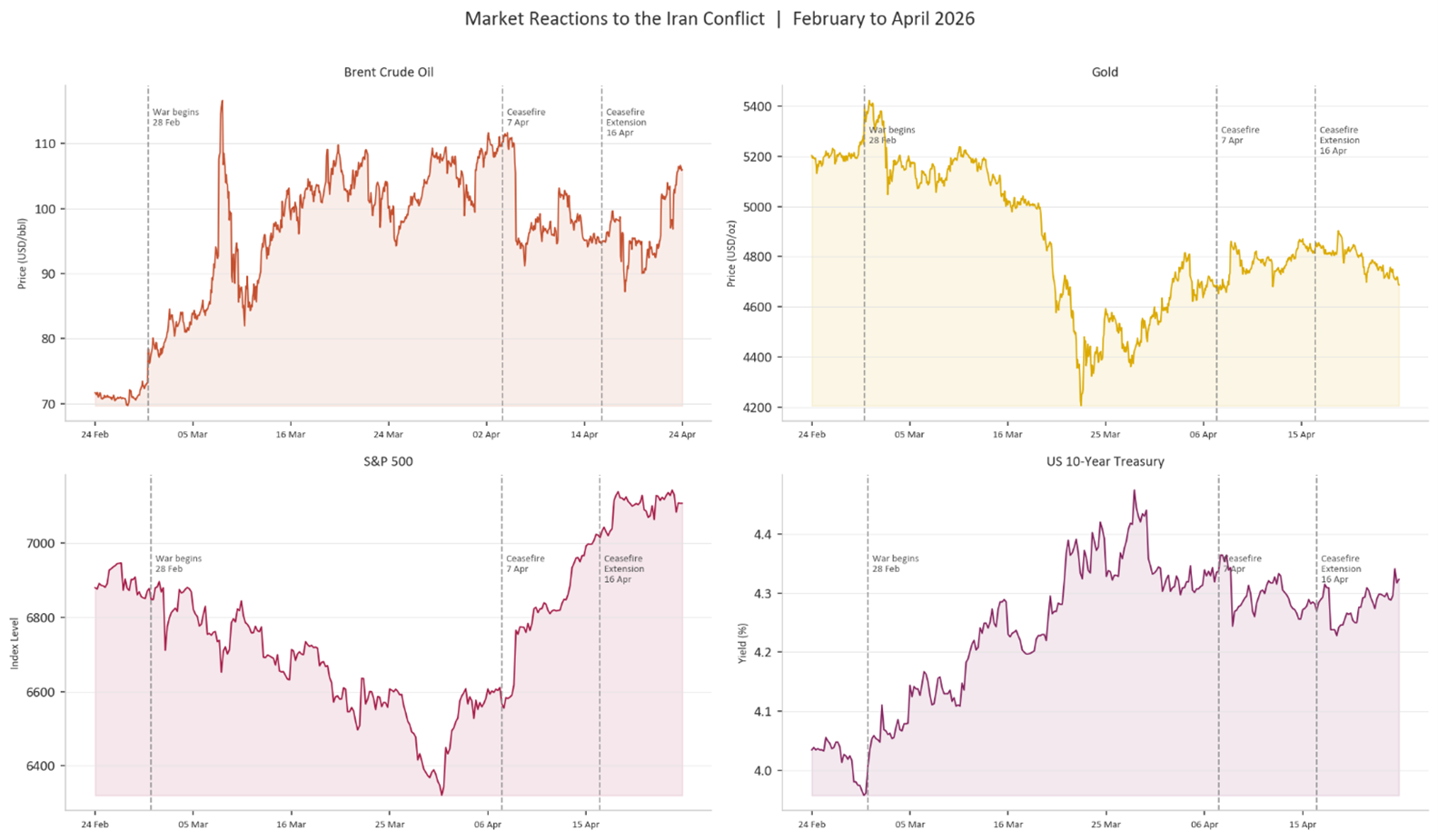

Chart 2

The period is best characterised as an exogenous shock, driven by geopolitical developments outside the scope of traditional economic modelling. Unlike endogenous market movements, where price action reflects changes in growth, earnings or monetary policy, this episode was shaped by external events and political signalling. Asset prices adjusted rapidly as markets attempted to incorporate shifting probabilities around supply disruption and inflation risk.

Late February and March were defined by escalating tensions, which drove a sharp rise in oil prices and a corresponding decline in equity markets.

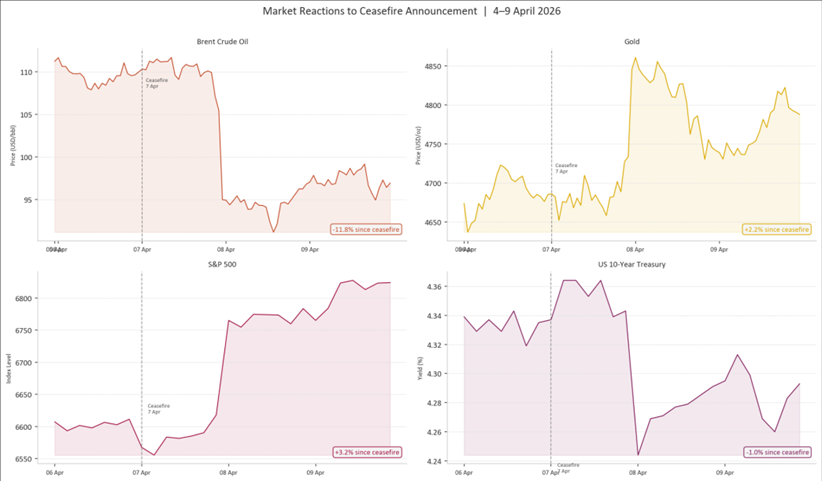

This dynamic reversed in early April. The announcement of a ceasefire on 7 April marked a clear turning point [see chart 2], triggering a rapid unwind of the geopolitical risk premium embedded in energy markets. Brent crude fell sharply, reversing a significant portion of its earlier gains.

This shift coincided with a recovery in equities, as easing inflation concerns and reduced supply risk allowed markets to move away from a defensive footing. Bond yields stabilised over the same period, reinforcing the view that inflation pressures had moderated, even if they had not fully dissipated.

Broadening participation

The recovery has been accompanied by a clear broadening in participation. While North America continues to play a central role, contributions from Emerging Markets and Asia Pacific ex Japan increased significantly in higher-risk portfolios.

This represents a healthier market dynamic than the more concentrated conditions seen previously. Rather than relying on a narrow set of drivers, performance has become more geographically diversified, reflecting improving confidence in the global outlook.

Intraday Volatility and Market Behaviour

Chart 3

Despite the more constructive backdrop, markets remain sensitive to geopolitical developments. Price action continues to reflect headline-driven moves, particularly in energy markets, with shifts in oil prices still influencing short-term risk sentiment. This creates a level of noise that can make short-term positioning challenging, even as the broader trend has improved [see chart 3].

Outlook

The key question going forward is whether this stabilisation can evolve into a more sustained recovery. A continued broadening in market leadership, particularly through Emerging Markets and Asia, would provide a more robust foundation for returns. However, the recovery remains dependent on a stable geopolitical backdrop. While the ceasefire has reduced immediate risks, underlying tensions have not fully dissipated. Any renewed escalation could reintroduce volatility, particularly through energy markets and inflation expectations.

Periods of geopolitical disruption can feel disorienting precisely because the source of uncertainty lies outside the economic system. However, the underlying principle remains unchanged. Diversification across asset classes, regions and risk factors does not eliminate short-term drawdowns, but it does provide resilience across changing market environments. Maintaining a disciplined, long-term approach remains key as markets transition from shock towards stabilisation.