A conflict without a clear endgame

It has been two weeks since the beginning of the joint US-Israel action in Iran, and there is as yet no clear end in sight, nor any coherent articulation of what the objectives and endgame of this action are.

The retaliation from Iran and its proxies has been swift and disruptive — one may argue that the response has, in effect, caused more sustained disquiet than the initial action itself.

Markets react as uncertainty deepens

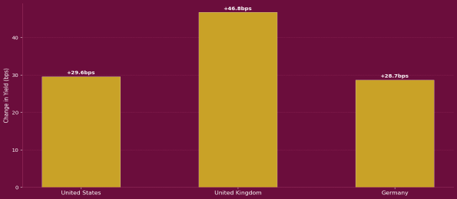

The market reaction, in and of itself, is not surprising. Fixed income markets — government bonds in particular — have repriced sharply, with yields rising materially, as shown in Figure 1.

Figure 1: Change in Government bond yields

It would be unwise, however, to read UK Gilt yields purely as a geopolitical signal: the UK sits at the conjunction of two structural faultlines — dependence on oil and gas imports from the Middle East and a persistently weak growth backdrop. Equity markets have, predictably, moved lower, as can be seen in Figure 2, with the notable feature that Japanese and European markets have declined by larger amounts than US equities — a direct consequence of their greater reliance on Middle Eastern oil flows relative to the US, which has materially increased its domestic production in recent years.

Figure 2: Change in global equity indices

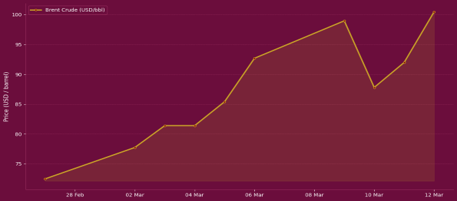

Brent crude, the primary Middle Eastern export benchmark, has gyrated sharply since the action began, exacerbated by the absence of any clear communication from the parties involved regarding objectives and desired outcomes. Some stabilisation has occurred following the IEA’s release of approximately 400 million barrels and the temporary lifting of Russian oil sanctions, but the trajectory from here remains uncertain.

Figure 3: Brent Crude prices

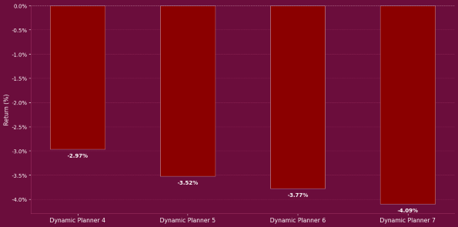

On the question of allocation performance, the period has produced negative returns across the benchmark profiles, as shown in Figure 4.

Figure 4: Performance of Dynamic Planner Benchmark Allocations

This is expected. The what-if analysis in our 3 March 2026 briefing drew on nearly three decades of market data to demonstrate precisely this: that a shock of this magnitude and velocity — combining an energy price dislocation, a repricing of sovereign risk and broad de-risking across equity markets — will produce short-horizon drawdowns. That is not evidence of structural failure; it is the predictable first-order consequence of the shock itself.

We have also observed VaR breaches in our daily monitoring, with a maximum of three daily breaches recorded in the Dynamic Planner 7 allocations.

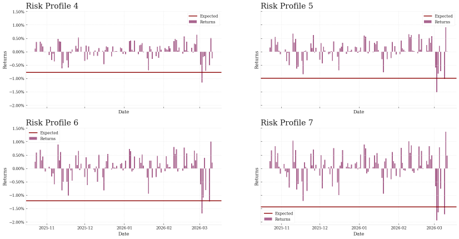

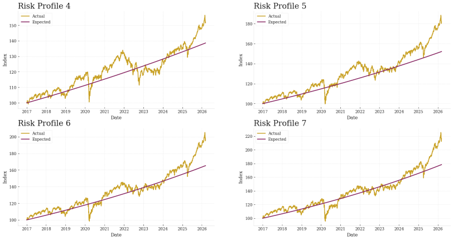

The gap between current performance and long-run expectations, visible in Figure 6, remains material — but the architecture is behaving precisely as designed.

Figure 5: Daily VaR

Figure 6: Performance vis-à-vis expectations

Fourteen days into the conflict, the situation in Iran remains unresolved, the energy complex volatile and the full ramifications of the opening strikes still partially obscured by the fog that always attends the early phase of a geopolitical rupture. The honest assessment is that further turbulence is probable before any durable stabilisation emerges. The performance shortfall visible in Figure 6 — allocations tracking below their long-run target in the immediate aftermath of the shock — is real, and warrants no minimisation.

What history shows in moments like this

Yet it is precisely here that the what-if scenarios in our 3 March 2026 briefing provide their most important counsel. That analysis asked a direct question of the historical record: how have these allocations behaved when energy markets, inflation dynamics and growth expectations move as they are moving now?

Nearly three decades of data gave an equally direct answer. They have held. The current episode remains entirely within the envelope of historical experience that the 3 March scenarios mapped — and the allocations are behaving accordingly.

Reaction is the risk, endurance is the strategy

In that same briefing, we wrote that the investors who fare worst in episodes of geopolitical stress are rarely those exposed to the initial shock; they are those who react to it. Reactive portfolio changes crystallise losses that time and compounding would otherwise recover. Those words bear repeating with greater force today. Every significant geopolitical rupture of the past half-century — 1973, 1979, 2003, 2008 — has eventually resolved, and in every case the assets that recovered were those that were held through the acute phase of the dislocation, not those that were sold into it.

The storm will pass. Markets have absorbed greater shocks than this, and the lesson across each episode has been consistent: the allocation that endured was the one that was allowed to endure. Remain invested. Trust the construction. Allow the architecture to do the work it was designed to do — and allow time to do what it has always done.