What advisers need to know

The joint US-Israeli military campaign launched against Iran on 28 February 2026 represents one of the most consequential ruptures in Middle Eastern geopolitics since the 2003 invasion of Iraq. Remarkably, it is the second such assault in less than nine months: the June 2025 twelve-day war, which included American strikes on the nuclear facilities at Natanz, Fordow and Isfahan, ended in a US-brokered ceasefire that proved, in retrospect, little more than an armed pause. Operations Epic Fury and Roaring Lion — targeting Iran’s nuclear infrastructure, ballistic missile programme, and senior leadership — have now fundamentally reordered the regional security architecture. The killing of Supreme Leader Ali Khamenei within hours of the opening strikes removed the central pillar of a theocratic order that had endured for four decades. What began as a pre-emptive strike framed around nuclear non-proliferation has rapidly acquired the character of open-ended conflict, with consequences for financial markets, with the energy commodity markets affected in particular. While the situation is a fast evolving one, we can already see the tremors rippling out across the globe.

Immediate Market Response

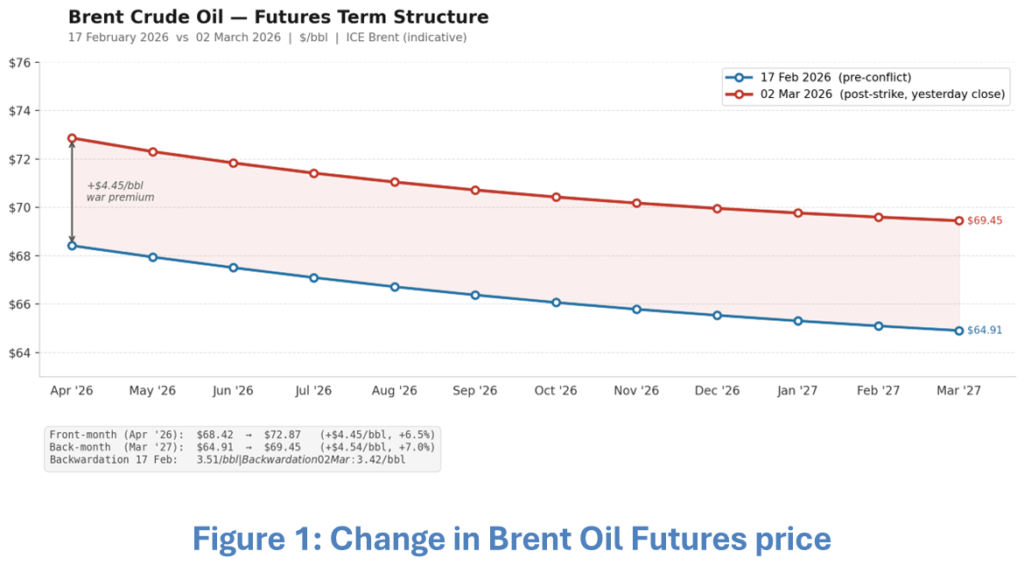

The most immediate market response to the conflict is legible in the Brent crude futures curve. By 17 February 2026, a geopolitical risk premium had already been partially absorbed into forward prices, reflecting the conspicuous five-week US naval buildup — itself a publicly declared act of coercive signalling rather than a covert operational preparation. The strikes of 28 February drove a further dislocation of approximately $4.50 per barrel at the front of the curve, compressing the term structure and steepening the backwardation as markets priced an acute near-term supply disruption rather than a structural long-run shock. The shift is illustrated in Figure 1. Yet the initial response understates the tail risk. A protracted conflict threatens a supply shock of historic proportions: sustained Hormuz disruption could drive Brent materially higher, with Gulf spare capacity effectively stranded and no adequate offsetting mechanism available.

The transmission channel extends well beyond flat price. The Strait has, in effect, closed itself through the withdrawal of commercial insurers rather than any formal act of interdiction: LNG carrier transits fell to zero on 1 March against eight the prior Sunday, VLCC rates struck an all-time record of $423,736 per day — a 94% move in 48 hours — and war risk cover lapses entirely on 5 March. The insurance market has rendered the arithmetic of transit commercially prohibitive before a single mine has been laid.

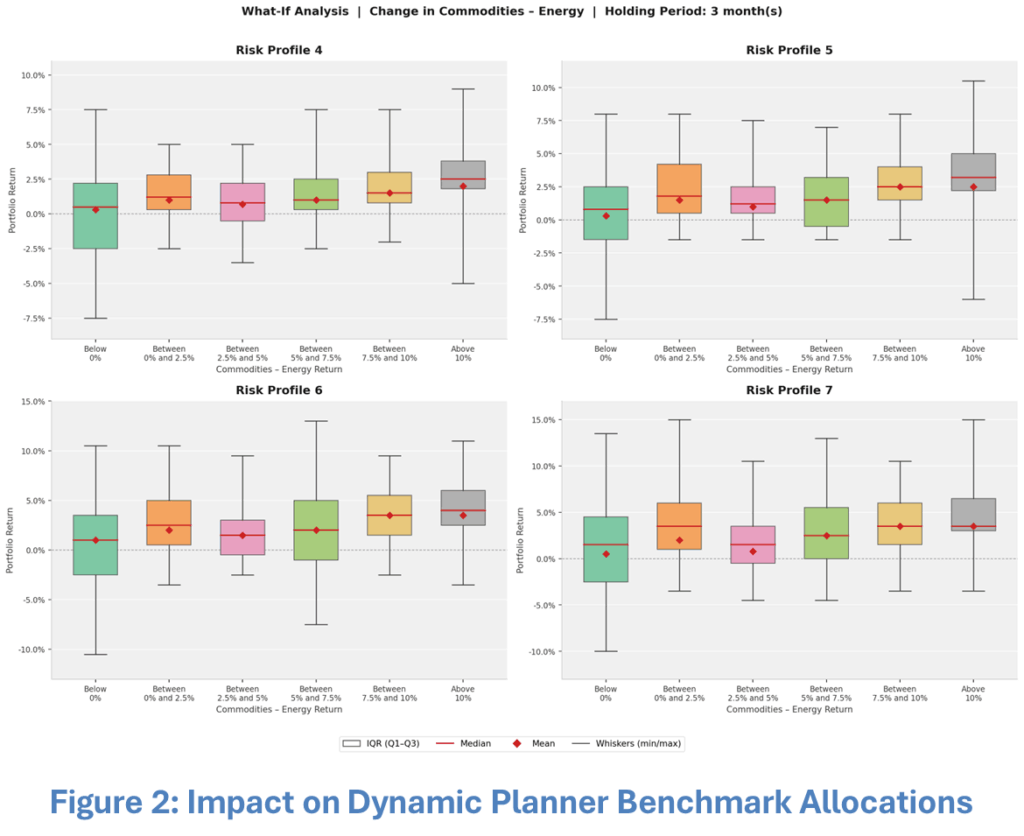

While none of the Dynamic Planner Benchmark allocations carry direct commodity exposure, the transmission effects of an energy price shock of this magnitude warrant careful examination. Drawing on historical data from January 1997 and applying a three-month holding period, we decompose portfolio performance across the full distribution of energy commodity return environments. The analysis is instructive: in aggregate, benchmark allocation returns have been positive across rising energy price regimes. The underlying dynamic is well-established — equity markets absorb an initial dislocation in the immediate aftermath of an oil price shock, but over a three-month horizon prices normalise and recover, with the diversification characteristics of the allocations providing ballast through the adjustment period.

Inflationary Transmission

In addition to the direct impact of oil prices rising, the inflationary transmission channel of an energy shock of this magnitude warrants careful examination. The historical precedents are unambiguous: the 1973 Arab embargo and 1979 Iranian Revolution each demonstrated how an energy price dislocation embeds itself in wage expectations, input costs, and services inflation, creating the self-reinforcing dynamic that monetary authorities find most difficult to extinguish. The post-Covid episode of 2021–2023 offers a more recent and structurally instructive parallel.

That inflation surge was a dual-channel event: supply chains dislocated by pandemic-era shutdowns and port congestion drove goods inflation to levels unseen since the 1970s, whilst the reopening demand surge collided with constrained energy production to push oil above $130 per barrel by March 2022. The lesson is that supply-side dislocations and energy price shocks are mutually reinforcing rather than independent — a dynamic directly relevant today.

The effective closure of the Strait of Hormuz has already produced both simultaneously: physical supply chains serving Asian manufacturers are severed at source, whilst the energy price impulse transmits immediately into shipping costs, petrochemical feedstocks, and food inflation. The transmission mechanism is broader and faster than a conventional oil price movement alone would imply. A sustained move toward significantly higher oil prices would arrive at precisely the moment when policy credibility is most fragile, threatening a renewed tightening cycle and compressing growth simultaneously. The stagflationary risk — the scenario that most challenges conventional portfolio construction by undermining the equity-bond negative correlation — cannot be dismissed.

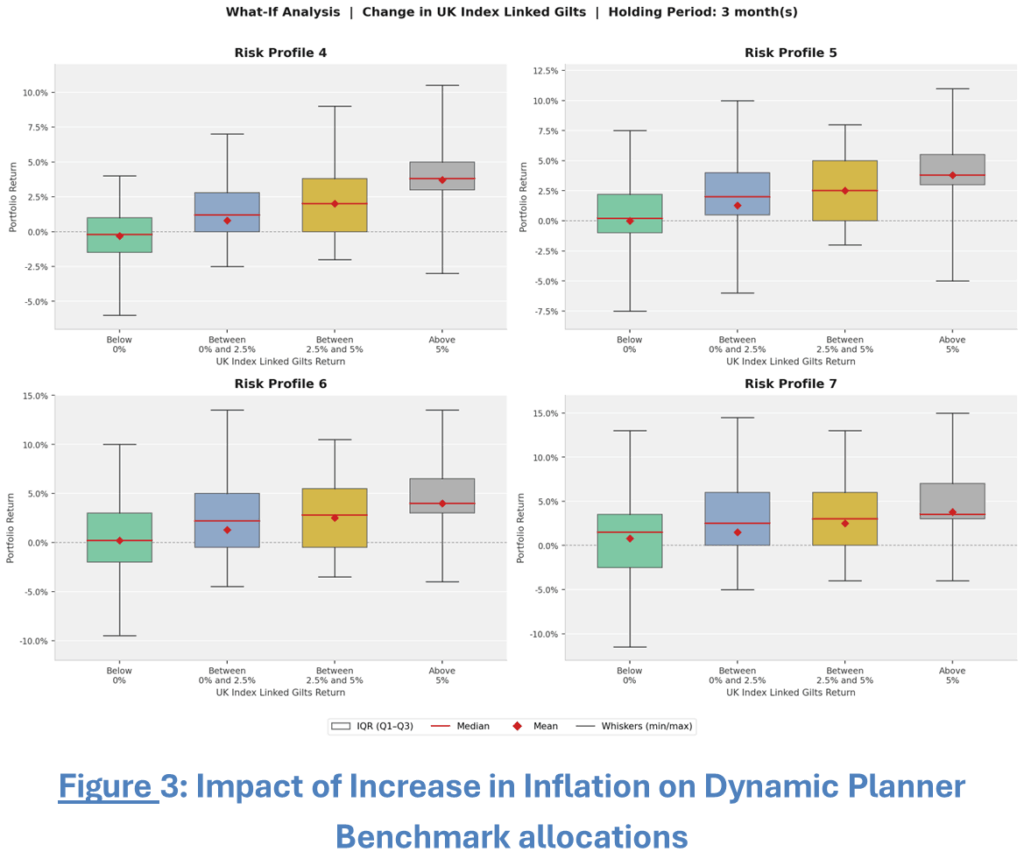

The natural hedge within the benchmark allocations is UK index-linked gilts, whose capital values adjust in approximate proportion to movements in the retail price index — a 1% rise in realised inflation implying a broadly commensurate appreciation in linker prices. The historical analysis in Figure 3 bears this out: across all four risk profiles, mean portfolio returns range from approximately 2% at Risk Profile 4 to 4% at Risk Profile 7 in the highest inflation bucket, with the distribution skewing further rightward as the inflation linkage compounds its stabilising effect across the three-month holding period.

Diversification and staying invested when faced with uncertainty

The events unfolding in the Middle East are consequential, and investor concern is entirely rational. Yet it is precisely for moments such as this that the Dynamic Planner benchmark allocations were constructed. Nearly three decades of market data — encompassing oil shocks, supply chain crises, geopolitical ruptures, and inflationary episodes — consistently demonstrate that diversification is not an abstract principle but a structural defence: equities absorb the initial dislocation, index-linked gilts hedge the inflationary consequences, and the breadth of the allocation ensures no single risk factor dominates the outcome. The most important counsel at a moment of acute uncertainty is also the most counterintuitive. The investors who fare worst in episodes of geopolitical stress are rarely those exposed to the initial shock — they are those who react to it. Reactive portfolio changes crystallise losses that time and compounding would otherwise recover. The situation in Iran remains fluid, but the architecture of these allocations was built to endure precisely that uncertainty.

Remain invested, maintain perspective, and allow the diversification to do the work it was designed to do.